How to Select the Best Financial Advisor

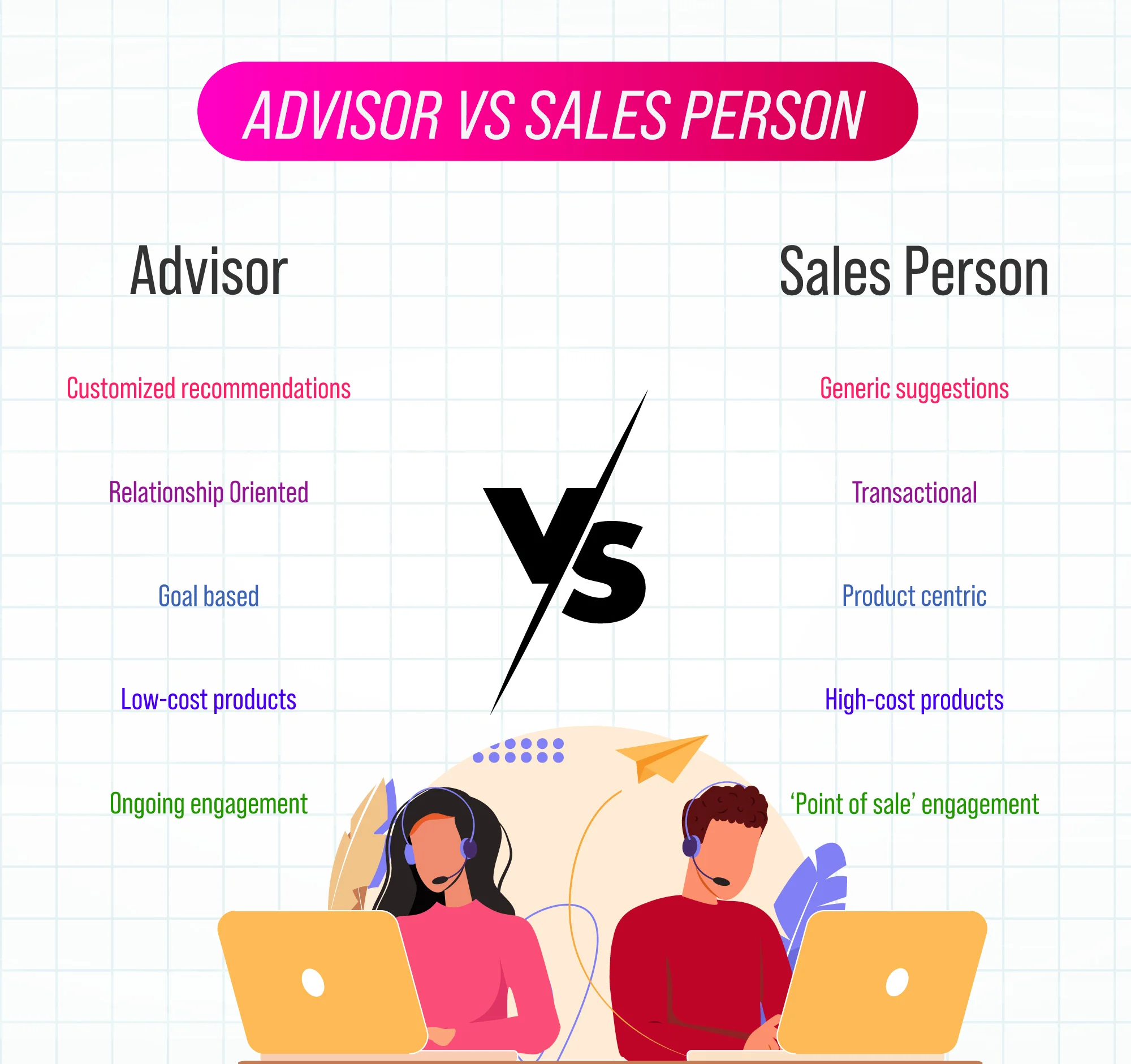

Is your Financial Advisor really just a skilled sales person?

A lot of so-called Financial Advisors today are really just sales people in disguise. Unlike a sales person, a great financial advisor will truly make an effort to understand your specific needs and customize your investing journey. Think about it - would you trust a doctor who recommends you an antibiotic without even assessing your symptoms?

Connect with the best Investing Experts!

What makes a great advisor?

What makes a great advisor?

A great advisor can make the difference between successfully meeting your financial goals or not. Remember, Investing is Easy, but creating wealth is not! The support of a qualified financial advisor can ensure that you not only invest in the right products, but with the right processes and mindset. As an investor, you should seek out the help of a qualified investing expert instead of taking financial advice from your friends and family, or from the internet or social media finfluencers. Here are some clear defining characteristics of a great financial advisor.

Understands your current financial situation and cash flows

A great advisor will begin with the basics – that is, by understanding where you stand today with respect to your finances, as well as assess your income and expenses and map your cash flows.

Customizes investing solutions as per your unique requirement

While sales people jump ahead to the recommendation stage and hurriedly pitch financial products, great advisors know that a one-size fits all approach doesn’t work when it comes to investing. Even two people of the exact same demographic and age can have completely different investing needs.

Sets the right expectations and manages investing behavior

The best advisor knows that the two things that can derail your investing journey are wrong expectations and behavioural traps. So, she makes an effort to help you properly understand risk/reward and also act as a behavoural coach during volatile markets.

Uses technology to enhance your journey

The best advisor will use technology to not just make your investing experience smoother and better, but to also make sure that the investment plan itself is highly customized.

Follows a strong, process led approach

The hallmark of a great financial advisor is making sure that all your investments are made using a process driven approach and are not ad hoc. For example, ensuring that high risk investments are made in a staggered manner, or that aggressive investments are systematically de-risked 12-18 months before your goal date arrives.

Displays high levels of client centricity

All things made equal, what differentiates an average financial advisor and a great financial advisor is their client centricity. The best financial advisor is one who cares about their clients to the extent that they would not suggest anything to their clients that they would not to their own family members! The best advisors will co-own financial goals with their clients and work to achieve them with complete dedication and with no conflict of interests.

Helps you invest with purpose!

The best advisors understand that investing with purpose leads to long term success. Rather than showcasing past returns and selling you products, they spend time in helping you define and prioritize your goals and invest according to them. The best advisors will ensure that you do not lose sight of your purpose throughout your investing journey

FAQs – Best Financial Advisor

What is the role of a financial advisor in financial planning?

The financial advisor plays a vital role in the financial planning process! In the long run, “how you invest” matters a lot more than “where you invest”. Even the best investment planning processes fail to deliver results if the “human element” is not managed properly. The best financial advisor doesn’t just recommend the best investment plans or suggest market related portfolio changes – she also plays the role of counsellor or behavioural coach to ensure that you remain steadfast on your financial planning journey!

Where can I get free financial advice?

You can get free financial advice from the internet or from social media finfluencers. However, this would be a huge mistake! Successful investing is all about customization, collaboration and joint decision making between clients and advisors. Relying on free, generic advice would almost certainly lead to a poor investing experience for you in the long run. When it comes to financial advice, don’t trust anything that is free and non-customized.

Can a financial advisor help me earn high returns?

The role of a great financial advisor isn’t to help you find the highest return products or to double your money. In fact, the best financial advisor is one who moves you away from this returns-centric mindset towards a more goal-centric mindset because doing so builds investing resilience and helps you benefit from long term compounding. Beware of so-called financial advisors who actually just provide stock tips and try to lure you with promises of high return investments! They are just wolves in sheep’s clothing.

How to select the best financial advisor?

The best financial advisor is one who follows a fantastic investing process that enables customization and collaborative decision making on your investments. They help you invest with purpose towards clearly defined goals. The best advisors also set the correct expectations and help you manage your behavioural traps effectively.