How to plan for your Child’s Higher Education

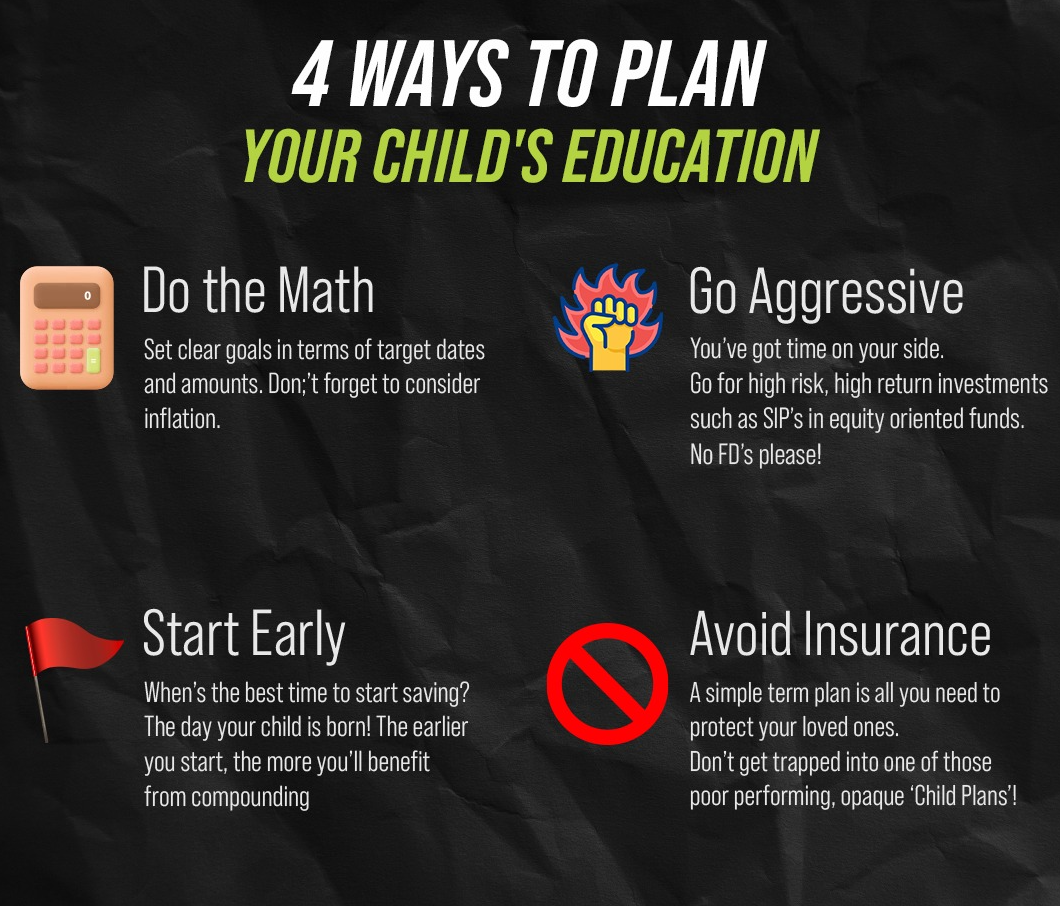

Like all parents, you most likely aspire to provide your child with a top-quality education. However, being able to successfully fund a great education for your kid requires advance planning, and the determination to stick to a long-term plan resolutely. Here are five important things for you to keep in mind.

Like all parents, you most likely aspire to provide your child with a top-quality education. However, being able to successfully fund a great education for your kid requires advance planning, and the determination to stick to a long-term plan resolutely. Here are five important things for you to keep in mind.

Inflation

While most goods and services are inflating at 6-7% per annum, the recent inflation trends in tuition costs has been closer to 9% - 11% per annum, depending upon the stream. What costs 5 Lacs today is likely to cost 20 Lacs or so after 15 years. Make sure you plan for the correct amount, while keeping inflation in mind. Consult a professional Financial Advisor if you’re confused about how to factor inflation into your long-term savings calculations.

Education = Earning Potential

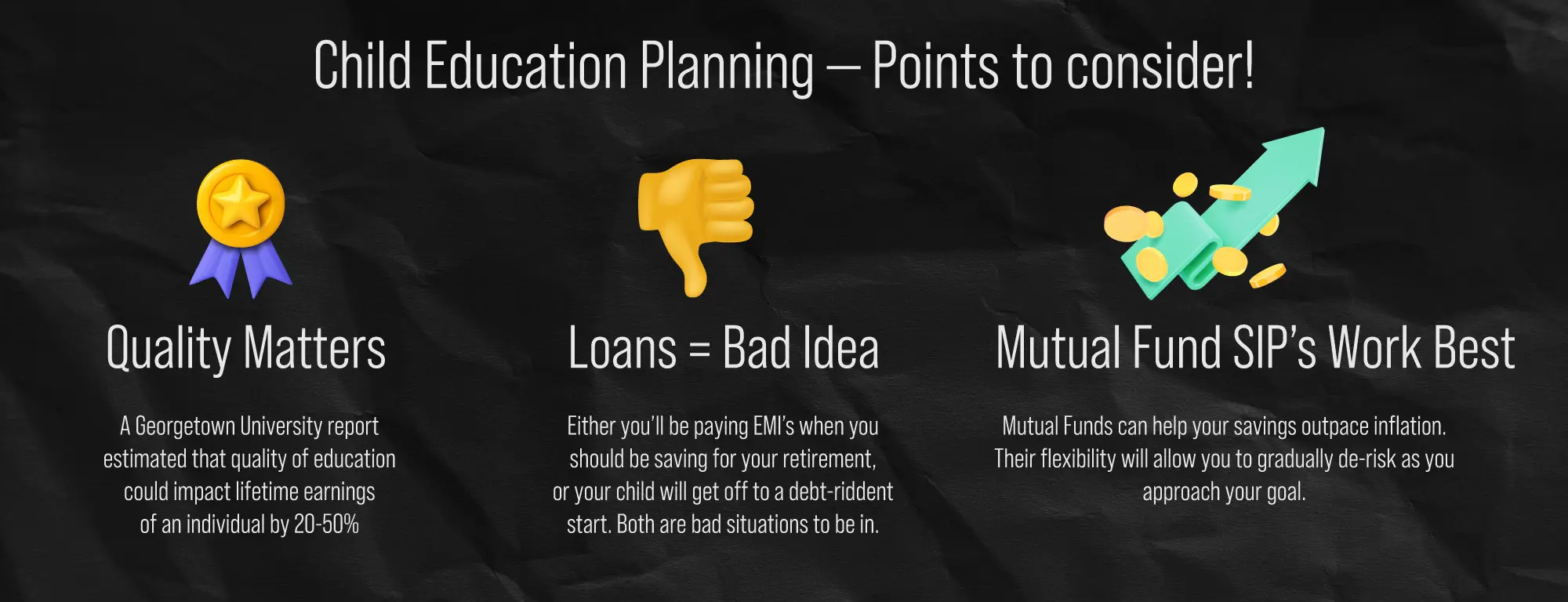

Studies have shown that the quality of education received by your child will impact her lifetime earnings by 25-50%. Over the course of one’s career, that’s a very large amount. As time goes on, it’s quite likely that the job environment will continue to become more hypercompetitive, with only the best educated students securing high quality placements. This makes it all the more important for you, as a responsible parent, to plan for your child’s education well in advance.

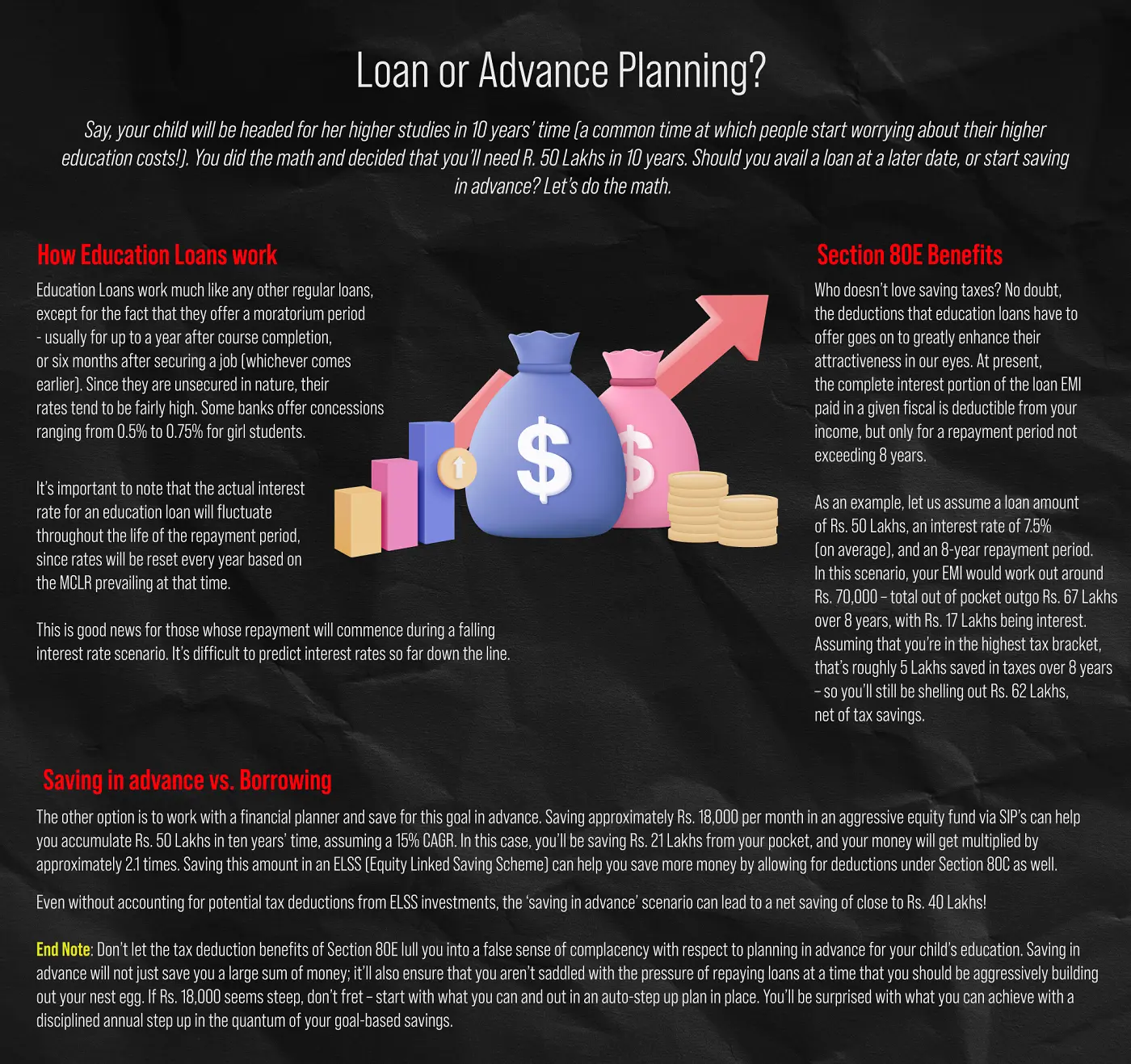

Student Loans = Bad Idea!

While sometimes it’s the only option, it’s not necessarily the best one. A thumb rule is that you or your child will need to repay one and a half times the loan amount over time. A debt-ridden career start could drive your child to take unwise and short term financial decisions. Although student loans do allow a full deduction of interest expenses incurred under Section 80E, the should still be looked at as a last resort.

Retirement first!

Your child could get through college using loans and grants, but you will never get your prime earning years back. Neither will anyone easily extend you a loan after you stop earning. Make sure you don’t lose sight of your own retirement, in the pursuit of creating a sufficient education fund for your child. Save for your Retirement first and your Child’s Education later.

Don’t fall into the Life Insurance Trap!

Mutual Funds offer a variety of products and solutions that could enable you to build a large enough corpus for your child’s education. You can run a long-term SIP Investment in an aggressive mutual fund during the initial years of your planning, and de-risk the corpus systematically using STP’s (Systematic Transfer Plans) a year or two prior to the goal date. In comparison, traditional savings plans such as fixed deposits and life insurance are inflexible, and also usually do not provide high real returns. Your Mutual Fund Advisor can help you with the best solutions and funds to help build a corpus for your child’s education, in light of your unique circumstances. Keep this in mind - because child education planning has an emotional angle to it, sales people play to this and often end up trapping unsuspecting investors in low return policies. Be careful!

Plan for your Child's Future!

FAQ’s – Child Education Planning

What is the right age to start a child education plan?

The earlier you start, the more you can benefit from compounding and create a large corpus without straining your wallet. The best time to start with a child education plan is the day your child is born. However, it really isn’t ever too late to start – your investing journey can be customized based on the number of years remaining, with a number of tools such as automated step ups or periodic lump sum injections.

Should I invest in a child plan from a life insurance company?

You should not invest in a child plan from a life insurance company. Unfortunately, these policies are the first to show up when you do a google search for ‘child education plan’, but that is only because insurers have paid for these searches. These child education plans are low return, very opaque and their features are often difficult to understand. Often, they don’t even beat inflation, let alone outpace it. Since education costs typically inflate at an above normal rate, this is obviously very detrimental.

How much money do I need for my child’s higher studies?

This would depend on a number of variables, such as your child’s age, aspirational degree, whether you’re looking at a domestic or foreign education, etc. It’s best to work with a qualified expert to map out this goal properly, factor inflation into the mix and arrive as a sustainable saving plan for it.

How can SIP’s help in child education planning?

SIP’s can be a powerful tool for child education planning because they allow you to invest small amounts every month in aggressive funds that can deliver high returns if you continue investing for the long term. However, SIP’s often fail without the support of a qualified expert because paper returns are very different from actual returns – the latter is going to be influenced by your investing behaviours!