Riding the SIP Wave: How to benefit from Volatile Markets

In recent months, equity mutual funds (especially SIP’s) have seen increased inflows and a renewed interest from the retail investor community. Whereas a lot of these SIP’s have been started with the intention of continuing them for 5 to 10 years or more, the truth is that not all of them will actually successfully complete their tenure. In this brief article, we’ll summarize a few key factors to keep in mind while planning for your future goals using SIP’s. Let’s begin with our “three golden rules” of SIP investing!

Rule #1: Rationalize your expectations. The rupee cost averaging benefit of SIP’s will absorb much of the risk associated with equity markets over the long term. Since risk and reward have an inverse correlation for long term investments, one must expect long term returns of no more than 12-14% CAGR from their equity SIP’s. Remember this is a GREAT post tax return to achieve compared to 6-7% post tax returns offered by other comparable monthly savings tools.

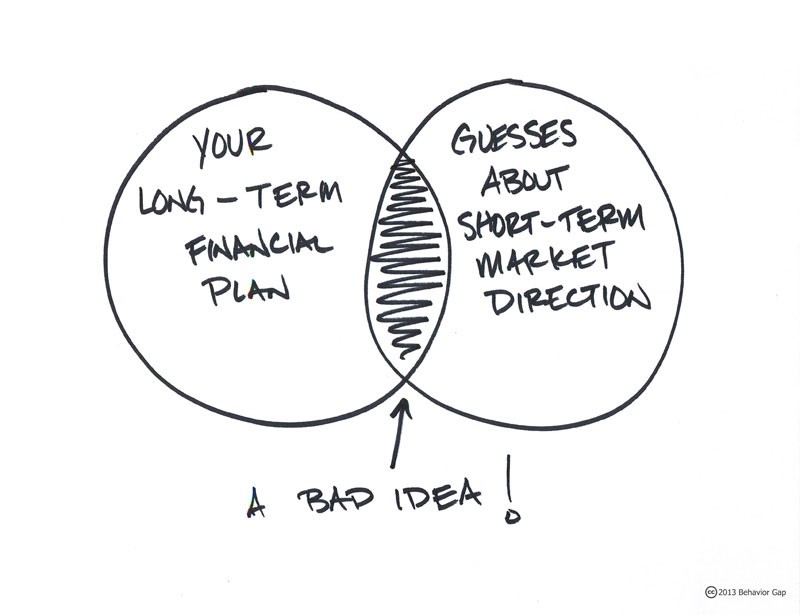

Rule # 2: Don’t time the market. Attempting to ‘time’ market cycles and moving in and out of SIP’s (based on your ‘judgment calls’ or tips from well-meaning friends) will almost certainly kill your SIP investment.

Rule #3: Stay put for the long term. One must start investing in equity SIP’s with the objective of keeping them going for at least 5 years or preferably even longer. Terminating them early could lead to losses in your portfolio.

What is Rupee Cost Averaging?

Rupee Cost Averaging is a wonderful risk mitigation mechanism exclusive to equity SIP’s. In theory, we all know that we should buy more of something when it’s cheap, and less of it when it’s expensive (Gold or Land, for instance). In real life and particularly in case of equity investments, emotions often lead us to do the exact opposite! By investing a fixed sum of money every month regardless of the price, you end up purchasing MORE during market downturns and LESS during good times. This ensures that the average buying price of your units is neatly averaged out, thereby providing you with stable growth over the long term.

How investors react to market cycles

|

“I buy on the assumption that they could close the market the next day and not reopen it for five years” Warren Buffett |

Media frenzy surrounding stock markets often leads investors to take irrational decisions based on the twin ‘value destroyers’ - greed and fear. It’s vital to insulate yourself from views of stock market ‘pundits’ who actually know very little about what’s going to happen tomorrow! Business news channels need to sensationalize market movements to generate ad-revenues, and this takes place at the expense of poor investors (who react to headlines such as ‘Bloodbath on Dalal Street’ with justifiable fear!) Ironically, the same investor rushes in to start new SIP’s when the headlines read ‘Nifty scales all-time high or ‘Euphoria on Dalal street!’ Both approaches are wrong.

As a result of the above, a large number of SIP’s land up getting terminated during the final months of bearish market cycles - and resume during the final months of bullish cycles. Common sense dictates that this is the exact opposite of what should be done. As a wise man once said, ‘a little bit of knowledge is a dangerous thing’!

By letting emotions cloud their judgment, investors often lose out on the real benefits of SIP’s. They continuously stop and restart their SIP’s - when the optimal strategy would be to just let them continue and allow market cycles to take their course. Investors who stopped their SIP’s and redeemed their money during the last market downturn (an astounding 16 Crore SIP accounts were closed in 2010-2011 in India!) lost out on the entire bullish cycle that commenced shortly thereafter.

Since one saves fixed sums of money in an SIP every month, the question of ‘timing the market’ shouldn’t arise. One must remain dispassionate towards market cycles when it comes to their SIP’s with the firm understanding that the magic of ‘rupee cost averaging’ is always at play.

Riding the SIP Wave

It’s time now to reveal the big secret behind successful SIP investing. And the secret is – that there IS no big secret! Just stick to the basics: ensure that you let your SIP’s get debited every month in a disciplined manner (just like EMI’s), don’t utilize long term funds for short term gratification unless it’s a dire emergency, and don’t let your emotions affect your decisions on stopping (or for that matter, starting!) your SIP’s. Allowing your SIP’s to flow - month in, month out throughout market cycles will ensure that you buy maximum units at the ‘point of maximum financial opportunity’ and the least units at the ‘point of maximum financial risk’. Your emotions will invariably push you to do otherwise! Don’t be swayed – ride the SIP wave instead.

An illustrative example

Here we present 5 year rolling SIP returns for a popular large cap equity fund launched in 1992 - UTI Equity Fund*. What’s worth noting is that there’s only one period (2004-2009) during which the SIP fared worse than a recurring deposit (that too because of the unprecedented global meltdown of 2008), and not one period during which the SIP generated negative returns! An interesting observation, given that markets have always remained volatile (and not always bullish). Had you stopped and started your SIP in the same fund repeatedly, chances are you’d make losses each time.

|

Period |

CAGR |

Rs. 5000 SIP yielded… |

|

2000-2005 |

31.45% |

654,925 |

|

2001-2006 |

40.66% |

810,020 |

|

2002-2007 |

39.71% |

792,566 |

|

2003-2008 |

42.69% |

847,895 |

|

2004-2009 |

3.63% |

333,958 |

|

2005-2010 |

20.40% |

502,497 |

|

2006-2011 |

20.18% |

500,977 |

|

2007-2012 |

6.66% |

360,008 |

|

2008-2013 |

14.78% |

439,611 |

|

2009-2014 |

12.93% |

420,218 |

In Conclusion

The key takeaway here is that dispassionate ‘savers’ always extract a lot more value from SIP’s than active traders. By committing yourself to riding the SIP wave for a long term horizon irrespective of market cycles, you’ll be stacking the odds heavily in your favour.

Let’s talk!

Want to know more about how to ride the SIP wave effectively? Speak to your Financial Planning Manager today.

Your Investing Experts

Relevant Articles

5 Behavioural Biases That Influence Our Investment Decisions

Human behaviour takes shape over a period of time based on various factors. Some of these include what we see, read, watch, and learn from people in our lives, television, social media, etc.

Chasing Returns vs. Wealth Creation

Creating Wealth from your investments is all about return maximization, right? Wrong! It may surprise you to know that your pernicious little habit of always trying to maximize portfolio returns may in fact be what is impeding your ability to generate long-term wealth. Here’s are four reasons why.

5 Behavioural Traps That Could Hurt Your Mutual Fund Investments

Learn 5 key biases impacting long-term mutual fund returns to boost your investment success.